Variable vs. Fixed: Where Things Stand Right Now

April 17, 2026 — Rate forecasts and market conditions can shift quickly. A new news cycle could change this outlook.

If you have a variable rate mortgage or HELOC, you’ve probably been watching the headlines and wondering what it all means for your rate. You’re not alone — I’ve had a lot of clients checking in over the past couple of weeks, and it’s a fair time to take stock of where things stand.

The rate gap today

The Bank of Canada’s policy rate sits at 2.25%, which translates to a prime rate of 4.45%. The gap between variable and fixed rates is one of the largest we’ve seen in recent memory — in many cases 0.60% to 1.00% lower for variable.

What’s shifting in the background

A weak labor market report this week lowered the probability of a Bank of Canada move at its next announcement on April 29. Market-implied odds sit at 6% chance of a cut and 94% chance of no change — so rates are expected to hold for now.

At the same time, inflation risks have increased, particularly tied to oil prices and global events. Inflation rising = upward rate pressure. Bond markets, which drive fixed mortgage rates, have already reacted. The result: fixed rates have been moving up while variable rates haven’t changed yet. Markets are pricing in roughly a 75% chance of a rate increase by end of 2026 — not certain, but worth paying attention to.

The math on a $300,000 mortgage

If you’re currently around 3.70% on a variable rate and comparable fixed rates are around 4.30%–4.40%, it would take roughly three 0.25% increases for those rates to meet. Each quarter-point increase adds roughly $100 to your monthly payment.

Locking in today means immediately stepping up to the 4.30%–4.40% range. One thing easy to overlook: fixed rates often move before the Bank of Canada actually acts. So by the time you decide to lock in, the rates available may already be higher than they are today.

Variable vs. fixed at a glance

Variable: starting around 3.70%, moves with Bank of Canada decisions, lower rate today, more exposure to future changes, historically saves more interest over the life of the mortgage.

Fixed: starting around 4.30%–4.40%, locked in regardless of what happens, no exposure to rate increases, you pay for the predictability upfront.

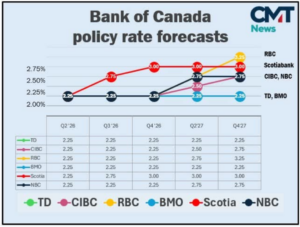

What the major banks are forecasting

Canada’s major banks aren’t aligned. TD and BMO forecast the policy rate holds flat at 2.25% through end of 2027. CIBC and NBC sit at 2.75%. Scotia forecasts 3.00% by Q4 2026. RBC is the most aggressive at 3.25% by Q4 2027. A 3.00% policy rate translates to approximately 5.20% prime — a meaningful difference from where we are today. (Source: CMT News)

Two questions worth asking yourself

How important is a stable, predictable monthly payment to you? If rates increased over the next year or two, would that impact your comfort level — financially or emotionally?

Variable rate strategy isn’t about timing the market perfectly. It’s about saving more interest over the life of the mortgage, even with some movement along the way. Fixed gives you stability at a higher starting cost. There’s no universally right answer — it depends on your situation, your timeline, and your risk tolerance.

Not sure what’s right for you?

I’m happy to talk through your specific numbers. Reach out anytime — no pressure, no one-size-fits-all answer.

This is a snapshot as of April 17, 2026. The rate environment has been moving quickly and the next few weeks of data and news could shift the picture.

Hi, I’m Jill, your mortgage pro. I am here to make the world of mortgages less confusing so you can feel confident in your financial decisions. Through my blog, I aim to provide you with the knowledge and guidance you need to make informed decisions. Your financial peace of mind is my top priority.